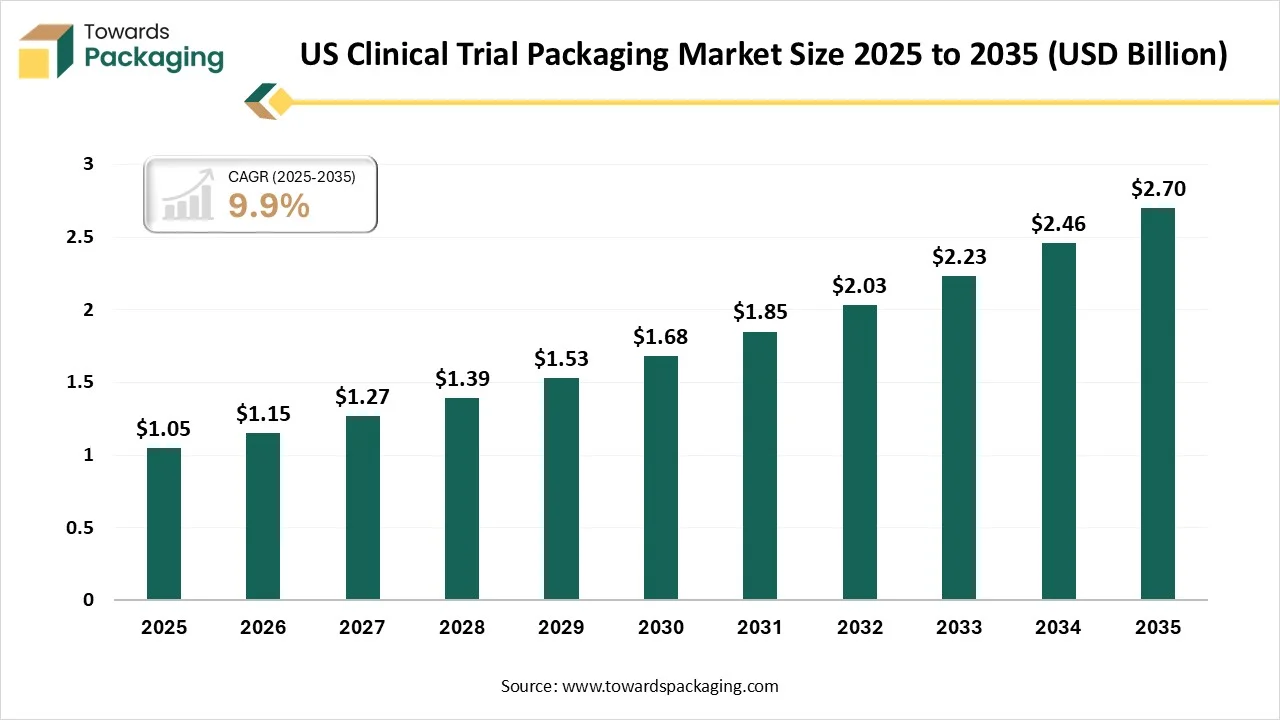

Ottawa, Feb. 26, 2026 (GLOBE NEWSWIRE) -- The global U.S. clinical trial packaging market size stood at USD 1.05 billion in 2025 and is projected to reach USD 2.7 billion by 2035, according to a study published by Towards Packaging, a sister firm of Precedence Research.

Request Research Report Built Around Your Goals: sales@towardspackaging.com

What is Meant by Clinical Trial Packaging?

Clinical trial packaging is a specialized process that involves designing, labeling, and assembling investigational medicinal products (IMPs) to guarantee safety, integrity, and compliance with regulations for study participants. This process includes creating, blinding, and packaging drugs in primary (direct contact) and secondary (outer) containers, often necessitating unique, multi-language, and tamper-evident labels to ensure the accuracy of the study.

What Are the Latest Key Trends in the U.S. Clinical Trial Packaging Market?

- Smart and Intelligent Packaging: Integration of technology like RFID, QR codes, and smart, connected devices is growing to improve real-time tracking, patient compliance, and supply chain visibility.

- Sustainability Initiatives: There is a strong, growing focus on developing sustainable, biodegradable, and eco-friendly packaging materials to meet environmental regulations and corporate social responsibility goals.

- Advanced Serialization and Security: Enhanced, sophisticated serialization methods are being adopted to ensure, in addition to regulatory compliance, improved drug traceability and protection against counterfeiting.

U.S. Government Initiatives for Clinical Trial Packaging:

- Decentralized Clinical Trials (DCT) Guidance: This FDA initiative provides a framework for shipping investigational products directly to participants' homes, requiring specific packaging to maintain stability and security during transit.

- Investigational New Drug (IND) Labeling Requirements (21 CFR 312.6): Mandates that all investigational drug containers carry the specific "Caution: New drug Limited by Federal (or US) law to investigational use" statement to ensure they are not confused with commercial products.

- Poison Prevention Packaging Act (PPPA) Compliance: This initiative by the Consumer Product Safety Commission (CPSC) requires child-resistant packaging for clinical trial drugs of high toxicity to prevent accidental ingestion by children in household settings.

- Good Clinical Practice (GCP) Modernization (ICH E6(R3)): An FDA-adopted initiative that encourages the use of innovative "smart" packaging technologies, such as digital monitors and electronic labels, to improve data integrity and participant adherence.

- Current Good Manufacturing Practice (cGMP) for Clinical Supplies (21 CFR 211): Establishes strict federal standards for the physical environment and documentation involved in packaging and labeling clinical materials to prevent cross-contamination or mix-ups.

- FDA Safety Considerations for Container Labels and Carton Design: Provides a structured approach to designing clinical labels—such as using "Tall Man" lettering and prominent dosage expressions—to minimize medication errors during trials.

- Bioresearch Monitoring (BIMO) Program: An FDA inspection initiative that audits clinical trial sites and sponsors to verify that packaging and labeling processes align with the study's protocol and maintain blind integrity.

- Quality System Regulation (QSR) for Investigational Devices: Under 21 CFR 820, the FDA requires that investigational medical device packaging remains legible and intact through all phases of distribution, storage, and use.

Get All the Details in Our Solutions - Access Report Sample: https://www.towardspackaging.com/download-sample/5977

What is the Potential Growth Rate of The U.S. Clinical Trial Packaging Industry?

The U.S. clinical trial packaging industry is growing rapidly due to increased investments in biopharmaceutical R&D, the expansion of complex clinical trials such as decentralized and adaptive designs, and the demand for specialized packaging. The growth is further driven by the rising popularity of biologics and advanced therapies, resulting in greater demand for temperature-controlled and high-barrier packaging solutions.

More Insights of Towards Packaging:

- Pharmaceutical Temperature Controlled Packaging Solutions Market Size, Trends, Segments, Companies, Competitive Analysis, Value Chain & Trade Analysis 2025-2035

- E-Commerce Packaging Market Size, Share, Trends, Segments, Regional Outlook (NA, EU, APAC, LA, MEA), and Competitive Analysis 2025-2035

- North America Stick Packaging Market Size and Segments Outlook (2026–2035)

- Hot Drinks Packaging Market Size, Trends and Regional Analysis (2026–2035)

- Recyclable Packaging Market Size, Trends, Key Segments, and Regional Dynamics with Manufacturers and Suppliers Data

- Reusable Packaging Market Size, Trends, Share, Trends, Segments, and Regional Insights (NA, EU, APAC, LA, MEA)

- U.S. Molded Pulp Packaging Market Size, Trends and Competitive Landscape (2026–2035)

- Vaccine Storage Packaging Market Size, Trends and Segments (2026–2035)

- Intelligent Packaging Market Size, Trends and Segments (2026–2035)

- Plastic Packaging Market Size and Segments Outlook (2026–2035)

- Lightweight Industrial Corrugated Packaging Market Size and Segments Outlook (2026–2035)

- Sustainable Aerosol Packaging Market Size, Trends and Segments (2026–2035)

- Poly-Woven Packaging Market Size, Trends and Segments (2026–2035)

- Mono-Material Cosmetic Tubes Market Growth, Trends & Forecast (2025-2035)

- U.S. Beer Packaging Market Size and Trend, Segment Outlook (2026–2035)

- Cold Chain Packaging Refrigerants Market Size, Trends and Segments (2026–2035)

- Packaging Adhesive Market Size, Trends and Regional Analysis (2026–2035)

- Heavy-Duty Corrugated Bulk Boxes Market Size and Segments Outlook (2026–2035)

- Next-Gen Paper & Fiber-Based Packaging Market Size, Trends and Regional Analysis (2026–2035)

- Flow Wrap Packaging Market Size, Trends and Competitive Landscape (2026–2035)

Segment Outlook

Material Type Insights

Which Material Type Segment Dominates the U.S. Clinical Trial Packaging Market?

The plastics segment dominated the market in 2025, driven by its lightweight, cost-effective, and durable properties suited for pharmaceutical applications. The demand is accelerated by the need for secure, contamination-resistant packaging for clinical trials, and the growing biotechnology sector in the U.S. Plastics & polymers hold the largest revenue share in pharmaceutical packaging, supported by high usage in thermoformed blister packs, bottles, and pouches.

The metal segment is projected to grow at the fastest rate in the market for the forecast period, driven by its superior barrier properties, durability, and protection against light and moisture. It is highly utilized in foil pouches and canisters to ensure product integrity. The demand for metal is increasing for specialized, high-protection applications. The need for high barrier protection, tamper-evident, and durable packaging for sensitive or high-value drug products in clinical trials.

Product Type Insights

How Did Vials and Ampoules Segment Dominate the U.S. Clinical Trial Packaging Market?

The vials and ampoules segment dominated the market in 2025, driven by the surging need for sterile, durable, and versatile primary packaging for biologics, vaccines, and injectable drugs. Their dominance stems from providing superior, contamination-free, and long-term stability for liquid and powder formulations in clinical studies. Vials and ampoules are essential for holding lyophilized, powder, and liquid medications, offering a secure, inert, and tamper-proof solution.

The syringes segment is projected to grow at the fastest rate in the market for the forecast period, driven by the rise in biologics and personalized medicine requiring precise, ready-to-administer doses. These, along with advances in cold chain logistics, are key factors in the growth of the pharmaceutical industry. A surge in clinical trials for biologics, vaccines, and gene therapies requires advanced packaging like prefilled syringes to ensure stability and safety.

Trial Phase Insights

Which Trial Phase Segment Dominates the U.S. Clinical Trial Packaging Market?

The phase III trials segment dominated the market in 2025, driven by the need for extensive, large-scale patient studies to secure regulatory approval. Because these late-stage trials require complex, high-volume, and often temperature-controlled packaging for thousands of participants, they account for the largest share of packaging demand. The need for specialized, tamper-evident, and compliant packaging for large-scale studies keeps this segment at the forefront.

The Phase II trials segment is expected to expand most rapidly in the market during the forecast period. This growth is fueled by heightened R&D investments in new treatments and a growing prevalence of chronic diseases that demand advanced, mid-stage packaging solutions. The complex, fast-paced, and patient-focused packaging requirements of Phase II trials are driving the most lucrative growth, especially for innovative, customized, and secure packaging designs.

End-User Insights

How Did the Clinical Research Organization Segment Dominate the U.S. Clinical Trial Packaging Market?

The clinical research organization (CROs) segment led the market in 2025, primarily due to rising outsourcing to Contract Research Organizations (CROs). These CROs have become essential in handling complex, multinational, and late-stage Phase III trials. This leadership is supported by a strong U.S. pharmaceutical R&D industry and strict packaging regulations. A key trend is the growing outsourcing for Phase III trials, driven by the demand for specialized, compliant packaging solutions.

The drug manufacturing facilities segment is projected to grow at the fastest rate in the market during the forecast period, driven by demand for advanced, secure, and compliant packaging solutions. This segment is increasingly adopting smart packaging to improve tracking and supply chain visibility, further contributing to its high growth rate. The growth is propelled by rising R&D investments in pharmaceuticals and biotechnology, the surge in chronic disease treatments, and the increasing complexity of clinical trials.

Recent Breakthroughs in the U.S. Clinical Trial Packaging Industry

In December 2025, Sesen, a provider of language services for the life sciences sector, introduced TrialS, an AI-driven platform designed for validating translations in regulatory, clinical, and labeling contexts. The platform's goal is to maintain consistency in clinical trial packaging and documentation by verifying content accuracy.

In July 2025, Radicle Science introduced its Radicle Discovery Gen 2 "Proof-as-a-Service" platform to aid the natural products and supplement industry in clinically verifying health claims. This platform leverages AI-powered virtual clinical trials, crowdsourcing, direct-to-consumer testing kits for nearly 100 physical biomarkers, and connects with wearables for data gathering.

Top Companies in the U.S. Clinical Trial Packaging Market & Their Offerings:

- Fisher Clinical Services: Provides end-to-end clinical supply solutions, including primary/secondary packaging and global cold chain logistics.

- Catalent, Inc.: Specializes in integrated clinical supply services with automated primary packaging for diverse dosage forms and kit design.

- PCI Pharma Services: Offers specialized packaging for biologics and advanced drug delivery systems with extensive cold chain support.

- Almac Group: Delivers flexible primary and secondary packaging alongside blinded clinical materials and "Just-in-Time" labeling.

- Sharp Services, LLC: Provides GMP-compliant primary packaging, clinical labeling, and specialized kitting for medical devices and pharmaceuticals.

- WestRock Company: Focuses on patient-centric adherence packaging and digital technologies to track dosing events and data accuracy.

- Amcor plc: Supplies innovative healthcare packaging materials like high-barrier laminates and sustainable, recyclable blister systems.

- Schreiner MediPharm: Specializes in smart labeling and functional solutions, including sensor-integrated packaging for real-time medication monitoring.

- Bilcare Limited: Offers research-based packaging design, comparator sourcing, and materials specifically engineered for product stability.

- Piramal Pharma Solutions: Provides integrated manufacturing and packaging for various dosage forms, including solid dose bottling and blistering for potent compounds.

Segment Covered in the Report

By Material

- Plastic

- Glass

- Metal

- Paper & Corrugated Fiber

By Product Type

- Vials & Ampoules

- Blisters

- Syringes

- Bags & Pouches

- Others (Bottles, Tubes, Kits)

By Clinical Trial Phase

- Phase III

- Phase II

- Phase I

- Phase IV

By End-User

- Clinical Research Organizations (CROs)

- Drug Manufacturing Facilities (Pharma/Biotech)

- Research Laboratories

Invest in Our Premium Strategic Solution: https://www.towardspackaging.com/checkout/5977

Request Research Report Built Around Your Goals: sales@towardspackaging.com

About Us

Towards Packaging is a global consulting and market intelligence firm specializing in strategic research across key packaging segments including sustainable, flexible, smart, biodegradable, and recycled packaging. We empower businesses with actionable insights, trend analysis, and data-driven strategies. Our experienced consultants use advanced research methodologies to help companies of all sizes navigate market shifts, identify growth opportunities, and stay competitive in the global packaging industry.

Stay Connected with Towards Packaging:

- Find us on Social Platforms: LinkedIn | Twitter | Instagram | Threads

- Subscribe to Our Newsletter: Towards Sustainable Packaging

- Visit Towards Packaging for In-depth Market Insights: Towards Packaging

- Read Our Printed Chronicle: Packaging Web Wire

- Get ahead of the trends – follow us for exclusive insights and industry updates:

Pinterest | Medium | Tumblr | Hashnode | Bloglovin | LinkedIn – Packaging Web Wire | Globbook | Substack | Bluesky | Justdial | Crunchbase | TrustPilot | Bizcommunity - Contact: APAC: +91 9356 9282 04 | Europe: +44 778 256 0738 | North America: +1 8044 4193 44

Our Trusted Data Partners

Precedence Research | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Healthcare Webwire | Packaging Webwire | Precedence Research Insights

Towards Packaging Releases Its Latest Insight - Check It Out:

Sugarcane-Based Packaging Market Size and Segments Outlook (2026–2035)

Composite Packaging Market Size, Trends and Segments (2026–2035)

Cohesive Packaging Market Size, Trends and Competitive Landscape (2026–2035)

Recyclable mono-material PE Market Size, Trends and Competitive Landscape (2026–2035)

Sustainable Wipe Packaging Market Size and Segments Outlook (2026–2035)

Seafood Packaging Market Size, Trends and Segments (2026–2035)

Tobacco Packaging Market Size and Segments Outlook (2026–2035)

Europe Pharmaceutical Packaging Materials Market Size, Trends and Competitive Landscape (2026–2035)

North America Tin Cannabis Packaging Market Size and Segments Outlook (2026–2035)

Semi-Automatic Stretch Wrappers Market Size, Trends and Competitive Landscape (2026–2035)

Cut Flower Packaging Market Size, Trends and Segments (2026–2035)

Clear Plastic Film Market Size, Trends and Competitive Landscape (2026–2035)

Edible Packaging Market Size, Trends and Regional Analysis (2026–2035)

Glass Packaging Market Size, Trends and Regional Analysis (2026–2035)

U.S. Rigid Thermoform Plastic Packaging Market Size, Trends and Segments (2026–2035)

Canada Plastic Packaging Market Size, Trends and Regional Analysis (2026–2035)

Packaging in Supply Chain Management Market Size, Trends and Segments (2026–2035)

North America Food Packaging Market Size, Trends and Segments (2026–2035)

North America Blister Packaging Market Size, Trends and Regional Analysis (2026–2035)

![]()